Investment Focus Areas

Based on its management philosophy, JIC provides risk capital to support corporate growth and enhance competitiveness through open innovation and investment in funds consistent with its principle of complementing the private sector

JIC makes investments in accordance with Investment Criteria* based on the Industrial Competitiveness Enhancement Act. In order to supply risk capital to the four investment focus areas designated by the Investment Criteria (listed below), JIC promotes open innovation in Japan through the establishment of investment funds, and contributes to enhancing Japan's industrial competitiveness and expanding the investment ecosystem.

Creating a positive cycle of domestic investment and innovation

To enhance Japan’s industrial competitiveness, support business activities that contribute to a positive cycle of domestic investment and innovation in industries requiring sustainable growth and demanding significant amounts of risk capital over a long period.

Creating and developing startups

To accelerate the creation and nurturing of startups, which are drivers of economic growth and innovation, and to foster the creation of global unicorns, support businesses that contribute to the development of the startup ecosystem.

Leveraging untapped regional management resources

Address the need for funding among local academic startups, leading medium-sized enterprises that possess technologies with high earning and innovation potential that are not being fully leveraged due to a lack of risk capital and human resources.

Promoting business consolidation in response to changes in market and business environments

Support enhancement of industrial competitiveness through medium- to long-term growth investments and industry consolidation in business fields that can adequately adapt.

Of these, the following three areas are designated as investment focus areas for LP investments in venture capital funds:

・Creating a positive cycle of domestic investment and innovation

・Creating and developing startups

・Leveraging untapped regional management resources

Approach to LP Investments in VCs

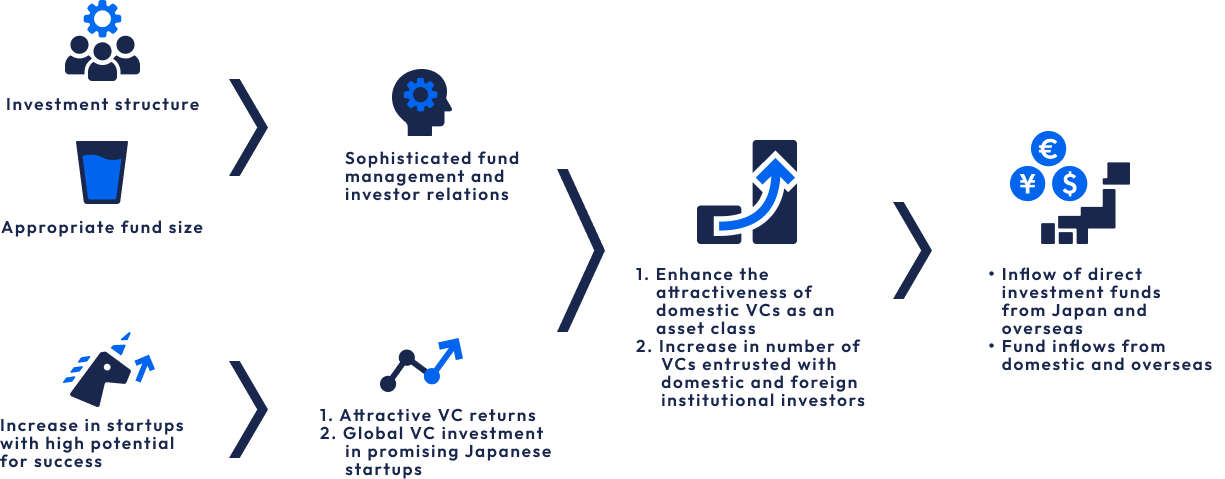

Compared to their counterparts in Europe and the United States, Japanese funds (especially VCs) receive less funding from institutional investors (pension funds, etc.), which is a significant challenge in terms of securing risk capital to support medium- to long-term growth. JIC supports the growth of Japanese fund managers who play a role in intermediating risk capital so that they can attract funds from Japanese and overseas institutional investors.

Increasing the supply of risk capital in the startup ecosystem

Simply increasing the supply of risk capital alone may lead to lower expected returns and make it difficult to achieve sustainable market growth.

Investment Themes and Initiatives to Date

Since 2021, JIC has progressively established investment themes by identifying areas in which private capital is insufficient, with a primary focus on priority investment areas.

JIC Investment Themes and VC Selection Perspectives (As of July 2025)

Investment Focus Areas under JIC’s Investment Criteria and Investment Themes

Creating and developing startups

Seed/Pre-Seed

- Invest in VCs that support startups in their earliest stages to broaden the base of startups capable of becoming future unicorns.

Aftermarket (VGI)

- Given the challenge of sustaining growth after listing, subsidiary VGI provides growth capital to post-IPO startups.

Early

- Support independent VCs with strong capabilities in providing hands-on guidance and leadership to establish a foundation for startup growth.

Secondary

- Support the development of secondary markets to avoid growth constraints on startups due to fund operational periods.

Growth

- Provide large amounts of risk capital to support the growth of growth-stage startups, where the number of players is limited and investment capital is scarce.

Go Global

- Support expansion into global markets, which is essential for nurturing unicorns.

(Support VCs with overseas bases and attract VCs operating globally)

Creating a positive cycle of domestic investment and innovation

Deep Tech

- Technologies with the potential to have a significant impact on resolving social issues through discontinuous innovation.

- Support for R&D and social implementation of technologies that require a long period of time and a considerable amount of capital from the research and development stage to market launch.

Life Science

- In addition to developing innovative new drugs through open innovation between startups and pharmaceutical companies, support innovation in the life science field, including pharmaceuticals, medical devices, health tech, and biotechnology.

Open Innovation

- Promote open innovation through business alliances between Japanese companies and startups with advanced technologies in the US, Southeast Asia, India, Israel, and other regions, and support the creation of innovative businesses.

Climate Tech

⇒ Expanding GX Target Areas

- Support the creation of innovative solutions and new businesses related to climate change, contributing to economic growth and decarbonization.

- Consider investing in funds targeting growth capital, buyouts, and infrastructure for domestic and international startups and mid-sized companies in the GX field.

Leveraging untapped regional management resources

Industry-Academia Collaboration

- Support research- and development-focused startups seeking to commercialize excellent technologies at local universities and other institutions that find it difficult to attract private investment.

- This will help foster startup ecosystems throughout Japan.

In addition, JIC has undertaken the following initiatives:

① Investments in emerging funds

② Development of VC as a foundation for risk capital circulation

③ Creating an environment that supports the emergence of mega-startups

Building on these efforts, JIC recognizes that further initiatives to support the growth of startups will continue to be important.

1

Emerging Fund Manager Program

Among the investment focus areas, we support private VCs (No. 1-3 funds) in areas where there is a shortage of capital supply or VC players

2

Monitoring VC Development

Expansion of the number and scale of VCs can be entrusted to institutional investors

3

Improving Environment for Creating Mega Startups

Support for building an ecosystem that enables startups to grow into large global enterprises

JIC Investment Guidelines:

Perspectives and Evaluation Criteria for Fund Selection

JIC has published investment guidelines summarizing the perspectives on suitability, expected performance, and governance of investee funds for LP investments in private venture capital and buyout funds. See below for details.

Investment guidelines

1

Structure and Organization

- The organization must be operated by a fully independent investment team, not a captive structure.

- The team must be dedicated to the fund business, without any other activities that could create a conflict of interest.

- The investment team should consist of full-time professionals whose sole responsibility is managing the fund, with no outside business interests that could create conflicts.

- The investment committee members should primarily consist of core members from the management company responsible for fund operations.

- The fund or investment professionals should have a track record that aligns with the fund's investment strategy.

- The standard carried interest rate should be 20%.

- Additional payment (interest charge) incurred by subsequent LPs should be fairly allocated to existing LPs who participated before the relevant closing.

- The European waterfall model should be the preferred distribution method.

4

Alignment and Governance

- The GP commitment, key persons, and allocation of carried interest should all be aligned and consistent.

- For managers with multiple funds employing distinct investment strategies, a clear allocation policy should be proposed.

- Conflict of interest matters should principally require approval from the advisory committee.

- An annual general meeting and advisory committee meeting should be held at least annually.

- Conduct fair value assessments.

(This includes fair value assessments of unlisted securities and the deduction of potential carried interest from LP interests in the capital account.)

- JIC's commitment as a proportion of the total among limited partners should principally be less than 50%, and any funds exceeding JIC's commitment amount should be raised from private investors.

- The managers must comply with JIC's requirement to form Code of Conduct / Code of Ethics (8 items) and Anti-Harassment Policy (10 items).

- The managers are required to establish and maintain a legal compliance system that meets key regulations, including the Financial Instruments and Exchange Act and anti-money laundering laws. Additionally, they must implement an effective information management system to properly safeguard personal and insider information.

- The fund size should principally exceed 6 billion yen.

If you have any questions about the above, please use the inquiry form below.

JIC Model Term Sheet

Purpose and Objective of this Publication

- Japan Investment Corporation (“JIC”) has been working to promote a virtuous cycle of risk capital.

- To achieve such a cycle, it is essential that sufficient funding be supplied to startups, particularly in their growth stages, and that capital from large-scale institutional investors be expanded. These priorities have also been emphasized in various recent government initiatives. As a government‑backed investment fund, JIC has been investing with the aim of expanding the number of VC firms that manage capital from institutional investors.

- As part of this effort, JIC has organized what it considers to be the key terms commonly required by institutional investors in limited partnership agreements (LPAs), and compiled them into the JIC Model Term Sheet.

- This Model Term Sheet follows the “Investment Guidelines” published by JIC in March 2025. While reflecting the fundamental investment principles set out in those guidelines, it focuses more specifically on contractual terms from the perspective of attracting capital from institutional investors—both domestic and international—who invest on a purely commercial basis. The purpose of this document is to clarify the principles that JIC considers essential for ensuring sound governance and achieving appropriate alignment of interests between the General Partner (GP) and Limited Partners (LPs).

- Investment in Japanese VC funds by domestic and overseas institutional investors remains limited. As a result, some LPAs contain contractual terms and conditions that may not be entirely favorable to LPs whose sole purpose is pure investment. JIC believes that publication of this Model Term Sheet will help expand institutional investor commitments to domestic VC funds, and ultimately contribute to the sustainable development of Japan's startup ecosystem.

Additional Notes on the Content

- This Model Term Sheet has been developed with VC funds in mind. While the fundamental principles—such as conflict of interest management, protection of LP rights, and information disclosure—remain largely consistent for investments in buyout and similar funds, the structure and content of the clauses are not necessarily identical due to differences in investment strategies.

- The purpose of this Model Term Sheet is to outline key contractual terms and conditions. The absence herein of any particular provisions does not imply that JIC considers them unnecessary. Furthermore, given the environment surrounding VC investments and market trends, it may be necessary to modify the contractual terms set forth in this Model Term Sheet or introduce new contractual terms.

- This Model Term Sheet may be revised or updated without prior notice to reflect actual practices, etc. When reviewing the content, please refer to the latest version available on JIC’s website.

- Please note that this Model Term Sheet intentionally omits any reference to tax-related matters. This is based on the understanding that tax treatment depends on an investor’s individual attributes and circumstances, and therefore should be considered on a case-by-case basis.

- GPs intending to seek investment from JIC are encouraged to prepare an LPA aligned to the principles of this Model Term Sheet in advance.